Focus group underway — contact us at info@nicksays.com to join.

Fair value is defined as "the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants..."

FASB ASC 820

Fair Value Compliance, Expertly Guided

A single-user workflow application for assembling the Level 3 inputs, assumptions, and estimates that drive valuation in non-publicly traded entities — the most difficult to audit and most time-consuming to analyze, document, and substantiate.

Rule 2a-5 (SEC's fair value rule) emphasizes the need for a strong, risk-based process that includes oversight, testing, and documentation.

SEC Commissioner Mark T. Uyeda — SIFMA Private Markets Valuation Roundtable, September 4, 2025

Workflow support software for fair value reporting under US GAAP and SEC Regulation S-X.

Key Benefits

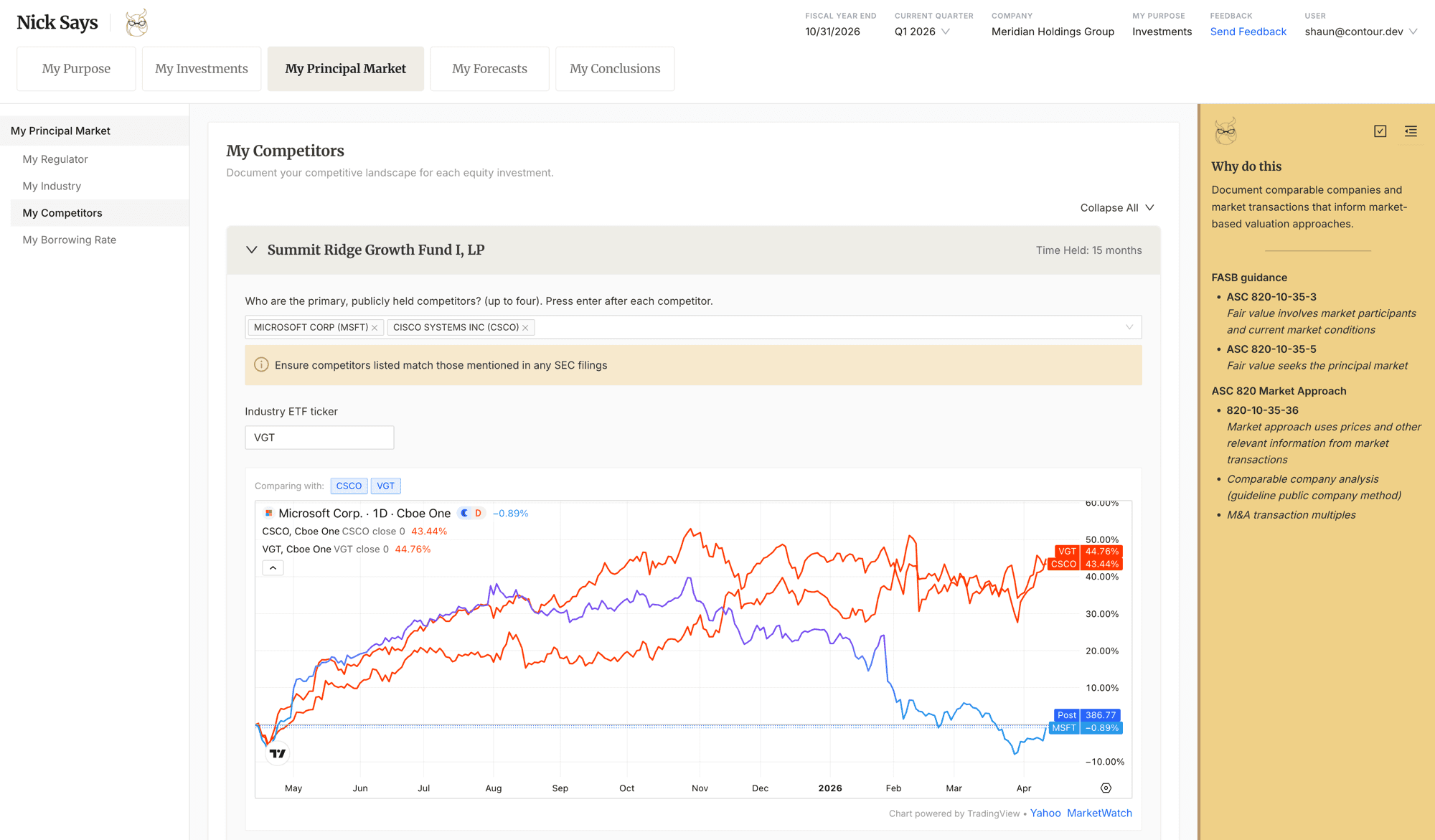

Document Evolving Fair Value Assumptions

Company-specific, Level 3 inputs require contemporaneous analysis of evolving market conditions.

Simplify Quarter-End Audit Review of Fair Value Estimates

Reduce the back and forth with audit teams through improved and ongoing tracking of company performance and forecasts.

Document with Confidence

Let the app do the heavy lifting of formatting, archiving, and tracking changes over time. You focus on gathering key information to support assumptions.

- 820-10-35-54A

A reporting entity shall develop unobservable inputs (Level 3) using the best information available in the circumstances, which might include the reporting entity's own data. A reporting entity shall take into account all information about market participant assumptions that is reasonably available.

- 820-10-55-22

A Level 3 input would be a financial forecast (for example, of cash flows or earnings) developed using the reporting entity's own data if there is no reasonably available information that indicates that market participants would use different assumptions.

- 820-10-50-2

A reporting entity shall disclose the following information: for fair value measurements categorized within Level 2 and Level 3 of the fair value hierarchy, a description of the inputs used.

Four regulatory paradigms requiring fair value — one software solution customized to each pathway.

Stock-Based Compensation

Support fair value reporting for stock options, RSUs, and warrants in VC-backed private companies. Complement your cap table management software with quarterly KPI tracking, calibration to recent funding rounds, and organized audit evidence for Level 3 assumptions.

Explore Options & RSUsGoodwill Impairment Monitoring

Efficient quarterly tracking of each reporting unit's performance with ongoing calibration to the original transactions that created goodwill. Shepherd data gathering for audit review and SEC disclosure narratives — reducing year-end scrambles for qualitative data.

Explore GoodwillPortfolio Mark-to-Market (ASC 946)

Investment company portfolio mark-to-market and NAV calculation support for privately held positions

Explore ASC 946ESOP Annual Appraisals

Support trustees and designated valuation advisors in year-end share appraisals — streamlining data gathering and key compliance needs for ERISA and IRC requirements, including Form 5500 reporting.

Explore ESOPDesigned for accounting and finance professionals navigating SEC, FASB, PCAOB, IRS, and DOL compliance requirements

Ready to Streamline Your Fair Value Process?

Bring structure, continuity, and a methodology record that holds up under review — every quarter.